Although we don't believe in timing the market or panicking over market movements, we do like to keep an eye on big changes -- just in case they're material to our investing thesis.

What: Shares of Nokia (NYSE: NOK ) have gotten clobbered today, down by as much as 12% after the Finnish smartphone maker reported first-quarter earnings.

So what: Revenue in the first quarter totaled $7.7 billion, which missed the Street's forecasts. On the bright side, the company narrowed its loss to $0.07 per share. There was other good news, as Lumia shipments were strong and increased 27% sequentially to 5.6 million units. Nokia closed the quarter with $5.9 billion in net cash.

Now what: Total smartphones dropped precipitously as Nokia expectedly ramps down Symbian units, which were just 500,000. The company's Asha line of feature phones saw shipments of 5 million. Nokia's lower-end devices are under competitive pressure from Android devices targeting low price points. The networks business held up, and CEO Stephen Elop said that segment helped contribute to Nokia's cash position this quarter. However, investors were focusing on the weakness up top.

Best Low Price Companies For 2014: Atlas Pearls and Perfumes Ltd (ATP)

Atlas Pearls and Perfumes Ltd, formerly Atlas South Sea Pearl Ltd., is an Australia-based Company. The Company is engaged in the business of pearl production in Indonesia and distribution globally through the Company�� marketing operations in Australia. The Company also manufactures and sells pearl jewellery primarily in Bali, Indonesia. It segments include Wholesale Loose Pearl and Jewellery. Its wholesale business is a producer and supplier of pearls within the wholesale market. The retail business is the manufacture and sale of pearl jewellery and related products within the retail market. The Company's subsidiaries include Perl��co Pty Ltd, Tansim Pty Ltd, P.T. Cendana Indopearls and Aspirasi Satria Sdn Bhd.

Best Low Price Companies For 2014: Sulliden Explorati Com Npv(SUE.TO)

Sulliden Gold Corporation Ltd., together with its subsidiaries, engages in the acquisition, exploration, and development of precious metal properties in Peru and Canada. It principally holds a 100% interest in the Shahuindo gold and silver project that comprises 26 mineral claims covering an area of approximately 7,358 hectares in the Cajabamba Province in northern Peru. The company was formerly known as Sulliden Exploration Inc. and changed its name to Sulliden Gold Corporation Ltd. in October 2009. Sulliden Gold Corporation Ltd. is headquartered in Toronto, Canada.

Asset Acceptance Capital Corp. engages in the purchase and collection of defaulted and charged-off accounts receivable portfolios from consumer credit originators in the United States. The consumer credit originators primarily include credit card issuers, consumer finance companies, healthcare providers, retail merchants, telecommunications, and utility providers, as well as resellers and other holders of consumer debt; private brokers; and debt resellers. The company periodically sells receivables from these portfolios to unaffiliated companies. It also finances the sales of consumer product retailers; and licenses a collection software application. The company was founded in 1962 and is headquartered in Warren, Michigan.

Best Low Price Companies For 2014: Merrimack Pharmaceuticals Inc (MACK.W)

Merrimack Pharmaceuticals, Inc., incorporated in 1993, is a biopharmaceutical company discovering, developing and preparing to commercialize medicines paired with companion diagnostics for the treatment of serious diseases, with an initial focus on cancer. The Company�� product candidates include MM-398, MM-121, MM-111, MM-302 and MM-151. As of June 31, 2011, the Company owned approximately 74% interest of Silver Creek.

The Company�� Network biology is an interdisciplinary approach to drug discovery and development that enables the Company to build functional and predictive computational models of biological systems based on quantitative, kinetic, multiplexed biological data. The Company provides its scientists with insights into how the complex molecular interactions that occur within cell signaling pathways, or networks, regulate cell decisions and how dysfunction within these networks leads to disease. The Company applies network biology throughout t he research and development process, including for target identification, lead compound design and optimization, diagnostic discovery, in vitro and in vivo predictive development and the design of clinical trial protocols.

MM-398

MM-398 is a stable nanotherapeutic encapsulation, or enclosed sphere carrying an active drug, of the marketed chemotherapy drug irinotecan. MM-398 achieved its primary efficacy endpoints in Phase 2 clinical trials in pancreatic and gastric cancer. In an open label, single arm Phase 2 clinical trial of MM-398 as a monotherapy in 40 metastatic pancreatic cancer patients who had previously failed treatment with gemcitabine, patients treated with MM-398 achieved median overall survival of 22.4 weeks. Additionally, 20% of the patients in this Phase 2 trial survived for more than one year, and the Company observed a disease control rate, meaning patients exhibited stable disease or partial or complete response to treatment, of 47 .5% at six weeks.

The Company focuses on ini! ti! ating a Phase 3 clinical trial of MM-398 for the treatment of patients with metastatic pancreatic cancer who have previously failed treatment with gemcitabine. The trial is expected to enroll approximately 250 patients and is designed to compare the efficacy of MM-398 as a monotherapy against the combination of the chemotherapy drugs fluorouracil, or 5-FU, and leucovorin. There are multiple ongoing Phase 1 and Phase 2 clinical trials of MM-398. In July 2011, the United States Food and Drug Administration (FDA) granted MM-398 orphan drug designation for the treatment of pancreatic cancer.

MM-121

MM-121 is a fully human monoclonal antibody that targets ErbB3, a cell surface receptor, or protein attached to the cell membrane that mediates communication inside and outside the cell, that the Company�� network biology approach identified as a target in a range of cancers. A monoclonal antibody is a type of protein normally produced by cells of the immun e system that binds to just one epitope, or chemical structure, on a protein or other structure. MM-121 is designed to inhibit cancer growth directly, restore sensitivity to drugs to which a tumor has become resistant and delay the development of resistance of a tumor to other agents. In collaboration with Sanofi, the Company focuses on testing MM-121 in combination with both chemotherapies and other targeted agents across a range of spectrum of solid tumors, including lung, breast and ovarian cancers. The Company partnered MM-121 with Sanofi after it initiated Phase 1 clinical development of the product candidate.

MM-111

MM-111 is a bispecific antibody designed to target cancer cells that are characterized by overexpression of the ErbB2 cell surface receptor, also referred to as HER2. A bispecific antibody is a type of antibody that is able to bind simultaneously to two distinct proteins or epitopes. The Company�� network biology approach identif ied that ligand-induced signaling through the complex ! of Erb! B! 2 (HER2)! and ErbB3 is a promoter of tumor growth and survival than previously appreciated.

MM-302

MM-302 is a nanotherapeutic encapsulation of doxorubicin with attached antibodies that are designed to target MM-302 to cells that over express the ErbB2 (HER2) receptor. The Company is conducting a Phase 1 clinical trial of MM-302 in patients with advanced ErbB2 (HER2) positive breast cancer.

MM-151

MM-151 is an oligoclonal therapeutic consisting of a mixture of three fully human monoclonal antibodies designed to bind to non-overlapping epitopes of the epidermal growth factor receptor (EGFR). EGFR is also known as ErbB1. An oligoclonal therapeutic is a mixture of two or more distinct monoclonal antibodies. The Company has designed MM-151 to block signal amplification that occurs within the ErbB cell signaling network. The Company has submitted an investigational new drug application (IND), to the FDA for MM-151 in July 2011.

Best Low Price Companies For 2014: Johnson Outdoors Inc.(JOUT)

Johnson Outdoors Inc., together with its subsidiaries, designs, manufactures, and markets seasonal outdoor recreation products used primarily for fishing, diving, paddling, and camping. Its Marine Electronics segment offers battery powered fishing motors for trolling or primary propulsion; sonar and GPS equipment for fish finding and navigation; downriggers for controlled-depth fishing; leisure boat navigation technology; and lake charts. The company?s Outdoor Equipment segment provides consumer tents, sleeping bags, camping furniture, and other recreational camping products; commercial tents, such as party tents and accessories, including lighting systems, interior lining options, and mounting brackets; heavy-duty tents and lightweight backpacking tents for the military, including modular general purpose tents, rapid deployment shelters, and lightweight one and two person tents; and military tent accessories, such as fabric floors, as well as field compasses and digital instruments, and performance measurement instruments. This segment also acts as a subcontract manufacturer for other providers of military tents. It primarily serves camping and backpacking specialty stores, sporting goods stores, catalog and mail order houses, general rental stores, and tent erectors. Its Watercraft segment offers canoes, kayaks, accessories, paddles, and personal flotation devices. The company?s Diving segment manufactures and markets a line of underwater diving and snorkeling equipment, including regulators, buoyancy compensators, dive computers and gauges, wetsuits, masks, fins, snorkels, and accessories for technical and recreational divers. This segment also offers diving gear to dive training centers, aquariums, and resorts. Johnson Outdoors Inc. operates primarily in the United States, Europe, Canada, and the Pacific Basin. The company was founded in 1985 and is headquartered in Racine, Wisconsin.

Best Low Price Companies For 2014: Regis Corporation(RGS)

Regis Corporation owns, operates, and franchises hairstyling and hair care salons in the United States, the United Kingdom, Canada, Puerto Rico, and internationally. It offers haircutting and styling, including shampooing and conditioning; hair coloring; and waving to men, women, and children. The company also owns and operates hair restoration centers, which provide hair systems, hair transplants, and hair therapy services, as well as hair care products. Its salons operate primarily under the Regis Salons, MasterCuts, SmartStyle, Supercuts, Cost Cutters, Sassoon, Promenade salons, Hair Masters, First Choice Haircutters, Magicuts, and Hair Club trade names in regional shopping malls, strip centers, lifestyle centers, Wal-Mart supercenters, department stores, mass merchants, and high-street locations. As of June 30, 2011, the company owned, franchised, or held ownership interests in approximately 12,700 locations. Regis Corporation was founded in 1922 and is headquartered i n Edina, Minnesota.

Advisors' Opinion: - [By Geoff Gannon]

For example, a company involved in a mundane business like running hair salons ��like Regis (RGS), dentist offices ��like Birner Dental (BDMS), grocery stores ��like Village Supermarket (VLGEA), or garbage dumps ��like Waste Management (WM), may be easy to estimate as essentially a no-growth business.

Best Low Price Companies For 2014: Ritchie Bros Auctioneers (RBA.TO)

Ritchie Bros. Auctioneers Incorporated, an industrial auctioneer, sells various equipment to on-site and online bidders. The company, through unreserved public auctions, sells a range of used and unused industrial assets, including equipment, trucks, and other assets utilized in the construction, transportation, agricultural, material handling, mining, forestry, petroleum, and marine industries. It also provides Internet bidding services, which facilitate customers access to live and online auction participation. The company primarily serves buyers and sellers of equipment, trucks, and other industrial assets; rental companies and brokers; finance companies; and truck and equipment dealers. As of December 31, 2011, it operated approximately 110 locations in approximately 25 countries, including 43 auction sites worldwide. The company was founded in 1963 and is headquartered in Burnaby, Canada.

Best Low Price Companies For 2014: Cross Country Healthcare Inc.(CCRN)

Cross Country Healthcare, Inc. provides healthcare staffing and outsourcing services to the healthcare market in Europe, the United States, Canada, and Asia. The company?s Nurse and Allied Staffing segment provides nurse and allied staffing services; healthcare professionals in various specialties, such as operating room and radiology technicians, rehabilitation and respiratory therapists, radiation therapy technicians, nurse practitioners, and physician assistants; and registered nurses, licensed practical nurses, and certified nurse assistants for per diem assignments. This segment markets its nurse and allied staffing services primarily to acute care hospitals, health systems, public and private healthcare facilities, and for-profit and not-for-profit facilities under the Cross Country TravCorps, MedStaff Healthcare Solutions, NovaPro, Cross Country Local, CRU-48, Allied Health Group, and Assignment America names. Its Physician Staffing segment offers temporary physici an staffing services. The company?s Clinical Trial Services segment provides contract staffing and outsourcing, drug safety monitoring, and regulatory consulting services to pharmaceutical, biotechnology, and medical device companies, as well as contract research organization customers under the ClinForce, Assent, and AKOS brands. Its Other Human Capital Management Services segment offers education and training, as well as retained search services primarily related to physicians, allied health, and healthcare executives. The company was formerly known as Cross Country, Inc. and changed its name to Cross Country Healthcare, Inc. in May 2003. Cross Country Healthcare, Inc. was founded in 1996 and is headquartered in Boca Raton, Florida.

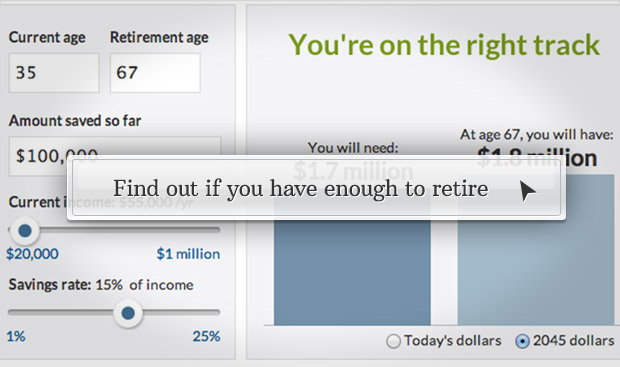

How I talk to my spouse about retirement

How I talk to my spouse about retirement  Reuters

Reuters

AFP/Getty Images How happy were markets that Washington made a deal? Almost as happy as the Afghanistan soccer team after beating Pakistan in August.

AFP/Getty Images How happy were markets that Washington made a deal? Almost as happy as the Afghanistan soccer team after beating Pakistan in August.